The Concentration Risk Trap: Why China-Centric Supply Chains Create Enterprise Fragility

When Efficiency Becomes Exposure: Reassessing China Concentration in a Structurally Volatile Era

Establishing supply chains between the US and China has proven to be relatively easy for most importers. This is largely not a testament to procurement professionals’ industriousness but instead is by design. China’s economic policies have intentionally centered around making trade between the US/China as competitive and frictionless as possible with massive infrastructure spend and the promotion of policies like rebates to spur low-cost exports.

However, despite rapid turnaround times on RFQ’s and perpetual supplier communication, what on the surface appears to be a highly efficient market is in many cases masking significant risk tied to market concentration.

Current Risk Landscape

China’s position as the “world’s factory” has made it the default supply chain platform for thousands of multinational firms. Its dense supplier ecosystems, vertically integrated component markets, and advanced infrastructure allow companies to move from sourcing to final assembly faster than almost any alternative geography.

This efficiency however creates a structural issue: concentration risk associated with single-country sourcing.

Tariffs are the most visible risk, but they are only one component of a broader and increasingly complex risk profile. The strategic question facing executives is not “Should we leave China?” but rather “What is our total risk exposure in China?”

The strategic question facing executives is not “Should we leave China?” but rather “What is our total risk exposure in China?”

For most companies, China will remain a key market over the next 5–10 years. However, the exact role China plays within their business will likely evolve based on risk factors and emerging opportunities in adjacent markets.

Below we highlight four leading risks impacting companies conducting business in China. It is only after assessing exposure across multiple dimensions can executives then determine which risks to retain and which to mitigate.

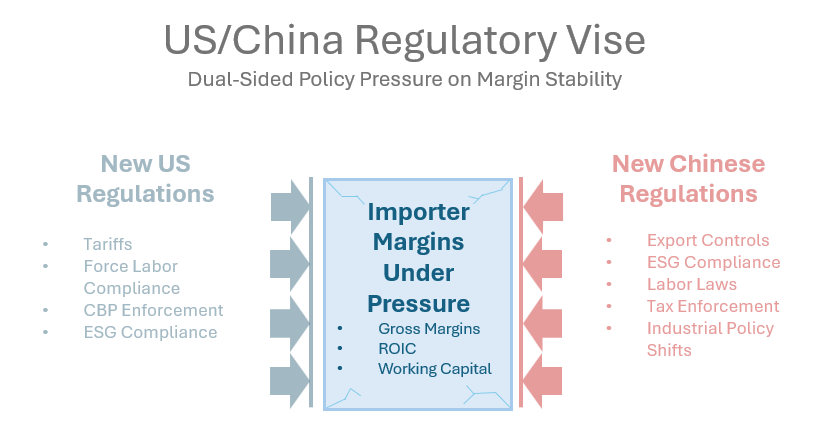

Regulatory Risk

Regulatory risk is one of the most impactful and difficult to understand risks for companies operating in Mainland China. Regulatory changes directly impact gross margins, operational flexibility, and in some cases even the ability to operate in the country as seen with high profile investigations and enforcement actions involving firms such as Bain & Company and PwC.

When assessing the regulatory environment, it is important to understand that new regulations are coming from both Chinese and US lawmakers. This creates a metaphorical regulatory vise for foreign companies operating in China.

Over the last fifteen years alone, Chinese suppliers themselves have faced increased regulatory requirements on everything from environmental standards to taxes to labor laws.

Studies during this period have indicated that enforcement of these new regulations have resulted in an average 30-40% increase in ex-works costs for Chinese produced goods- a cost which in many cases is directly passed along to US importers.

And while increased regulations and enforcement by the Chinese authorities raise costs for domestic manufacturers, the US regulatory landscape is equally impacting the economics around importing from China.

President Trump’s first and second terms have brought trade policy to the forefront, with tariffs appearing unexpectedly and at both arbitrary and punitive levels.

But beyond tariffs, the US has already been increasing regulatory scrutiny on companies active in Mainland China for some time. The Uyghur Forced Labor Prevention Act has materially increased documentation requirements and detention risk at U.S. ports, transforming compliance from administrative overhead into a supply chain gating mechanism.

More recently, semiconductor-related export controls have restricted U.S. firms which in turn has prompted retaliatory regulations from China around critical inputs, contributing to downstream bottlenecks.

As executives seek to handicap their regulatory risk in China, the long-term trajectory is clear: regulatory complexity is increasing, enforcement intensity is rising, and friction in cross-border trade is structurally higher than it was in previous decades.

For firms heavily concentrated in China, regulatory friction is no longer episodic — it is structurally embedded in the operating environment.

Geopolitical Conflict

Armed conflict across the globe has impacted trade routes in the Red Sea and resulted in embargoes preventing the flow of goods across once open borders.

When companies operating in China seek to assess their risk profile, the Taiwan question remains an ever-present threat. Will China forcefully unify Taiwan with the Mainland as President Xi espouses, and if so, when?

While no one can predict timing or how China will address what Beijing considers a core sovereignty issue, businesses reliant on China for production and consumption will experience impacts ranging from the extreme to the existential.

As a base case, most assume the Taiwan Strait will be restricted for commercial vessels. As of 2022, over $2.4 trillion dollars in annual sea shipments pass through this contested waterway. If war were to break out, anticipate surging insurance costs by carriers and potential logistics disruptions measured in months not weeks.

Beyond obvious impacts on the Taiwan Strait, the larger question then becomes does the international community enact strict trade restrictions on China during a conflict with Taiwan, and could this military incursion cascade to wider or even hotter conflict with neighbors such as Japan or worse yet, the United States.

In these scenarios, US importers sourcing critical inputs from China would be jolted from a Time to Recover stance common with traditional supply disruptions to a Time to Survive posture.

In these scenarios, US importers sourcing critical inputs from China would be jolted from a Time to Recover stance common with traditional supply disruptions to a Time to Survive posture.

Furthermore, while Taiwan represents the highest-severity flashpoint, China’s tensions with India and Japan introduce additional, lower-probability but still disruptive scenarios. Even limited confrontations can trigger insurance spikes, rerouting costs, export controls, and retaliatory trade measures.

These smaller skirmishes, while less headline grabbing, can also result in short-term though largely unpredictable disruptions.

From an executive’s perspective, these geopolitical conflicts cannot be treated as a binary global event where all firms are impacted equally. Exposure is company-specific — determined by revenue mix, production footprint, and dependency concentration.

Economic

After decades of rapid GDP expansion, China is now facing structural headwinds including slower growth, elevated debt levels, and real estate volatility with broader macroeconomic implications.

From a practical perspective, the greatest economic risk for foreign companies operating in China is generally tied to supplier solvency and unanticipated closings.

One week, engineers are reviewing tooling modifications with a critical supplier; the next, the factory gates are locked without notice and importers are scrambling to requalify tooling elsewhere.

This is a real risk to foreign companies with supply chains in China as financial transparency among mid-sized Chinese manufacturers can be limited, making it difficult to detect early signs of distress, especially amidst declining export demand.

Additionally, there is a scenario where companies in China may face a paradoxical environment: persistent overcapacity and pricing pressure in certain sectors due to overinvestment, alongside structurally rising labor and compliance costs.

For companies operating joint ventures or wholly foreign-owned enterprises in China, these forces can compress return on invested capital. These pressures appear structural rather than purely cyclical. In turn, these economic forces mean prolonged margin pressure becomes a balance sheet concern — not just an operating one.

Demographic

Another structural risk for companies operating in China is one of demographics. Since China’s accession to World Trade Organization in 2001, the country has relied on a large, increasingly skilled — and critically, low-cost labor force to power its manufacturing ascent.

China’s historic competitive advantage in labor cost is eroding — not only due to domestic wage inflation and demographic contraction, but also because alternative manufacturing hubs such as India and Vietnam are scaling with materially lower wage bases and increasing technical capability.

In sectors where labor remains a significant share of total cost, the differential between coastal China and emerging South or Southeast Asian markets has narrowed the case for single-country concentration.

China Population by Age

India Population by Age

As a result, while automation and moving up the value chain may partially offset this shift, manufacturers should anticipate higher wage floors, longer hiring cycles, and intensified competition for skilled labor.

In parallel, many privately owned Chinese manufacturers are undergoing generational transition. Founder-operators who built businesses during China’s export boom are increasingly transferring ownership to second- or third-generation successors who may even reside outside the country.

The incentives of these successors can differ materially from those of founding operators. In some cases, priorities shift from operational expansion to asset monetization.

For manufacturers located in rapidly urbanizing regions, underlying land values can exceed the operating value of the manufacturing business itself. This dynamic increases the probability of plant closures driven by rising real estate values rather than operating distress.

Taken together, demographic contraction and ownership transition suggest that China’s competitive model is evolving away from pure labor arbitrage. Companies that are heavily reliant on legacy cost assumptions should anticipate continued wage inflation, tighter labor markets, and greater operational volatility — reinforcing the need for efficiency-driven operating models rather than cost-driven ones.

Understanding the risk is one thing—executing diversification is another.

Exposure Framework

Many companies are aware of these risks. Assessing actual exposure, however, is a fundamentally different exercise. Executives can use the following questions to conduct a quick high-level check of their exposure to China-specific risks:

Supply Concentration

-

What percentage of total COGS is directly or indirectly dependent on China-based production?

-

What percentage of Tier-2 and Tier-3 suppliers are located in Mainland China?

-

How many sole-source components are manufactured exclusively in China?

Financial Resilience

-

What level of annual cost inflation (labor, compliance, tariffs) can your current gross margin absorb before EBITDA compression becomes material?

-

What is the working capital impact of a 90-day shipping disruption?

-

What percentage of revenue depends on China-based production?

-

What is the balance sheet impact if a China-based WFOE or JV were impaired?

Operational Continuity

-

What is the Time to Recover for your most critical China-sourced product?

-

What is the Time to Survive without China-based production?

-

How many months of inventory coverage exist for China-dependent SKUs?

-

Have alternative suppliers been qualified, or merely identified?

Strategic Dependency

-

Does China represent both a production base and a key end market for your revenue?

-

Would diversification meaningfully impact your competitive positioning?

-

Are switching costs operational, contractual, or regulatory in nature?

This is not a full risk audit — it is a board-level exposure screen. Companies that cannot confidently answer these questions likely lack sufficient visibility into their true concentration exposure.

As a directional benchmark, if more than 50% of COGS, revenue, or critical components are China-dependent, the business likely carries material single-country concentration risk.

If your inventory policy for China-sourced critical components mirrors that of non-critical inputs, or if secondary suppliers are merely qualified on paper rather than operationally proven, then your organization is not mitigating risk — it is performing risk management theater.

Once exposure is understood, the next question becomes magnitude: how does concentration risk manifest itself on the P&L and balance sheet?

Impact

Impact ranges from acute continuity disruptions to chronic margin compression, affecting both operational resilience and long-term profitability.

In a China–Taiwan conflict scenario, impact would likely be immediate and operationally severe. Closure of key trade routes such as the Taiwan Strait could disrupt shipments for months, strain working capital, increase insurance and freight costs, and force rapid inventory and sourcing adjustments.

Regulatory risk creates both chronic cost inflation and episodic escalation. Over time, increased compliance requirements raised baseline operating costs. However, abrupt policy shifts — including tariffs, export controls, or import restrictions — can materially alter cost structures with limited lead time.

In both cases, companies should prepare for structurally higher compliance costs and increased budgeting uncertainty driven by trade policy volatility.

As for the economic and demographic risks, the impact here is structural and less noticeable on a day-to-day basis but compounding continually. These pressures erode the cost advantage that historically justified high geographic concentration and often with limited offsetting levers.

Firms that diversify into lower-cost emerging markets such as India and Vietnam may achieve structural cost advantages in labor-intensive sectors. China’s risk-adjusted return profile meanwhile has shifted relative to the early globalization period.

This however does not imply withdrawal. Instead it requires deliberate risk allocation — understanding which exposures are strategic, which are tolerable, and which should be mitigated through diversification or structural hedging.

Mitigation

After risks are identified and impact assessed, companies must determine which exposures to transfer, which to mitigate, and which to retain. Below we highlight some common tactics currently in use:

Transfer

Most enterprise-level companies have been employing a multifaceted approach to risk management in China. Larger importers are transferring tariff risk to foreign suppliers through well-crafted Terms and Conditions. Additionally, these companies are including clauses pegging volatile commodity prices and currencies to international exchanges to improve financial forecasting.

These revised Terms and Conditions help reduce the impact of unanticipated tariff hikes and outsized commodity moves on P&Ls.

It is important however, to note that many small and mid-sized suppliers in China operate on tight margins. While proper Terms & Conditions can provide peace of mind, enforcement can be challenging, and in extreme circumstances enforcement could even threaten a supplier’s ability to continue operating.

Risk Mitigation

Beyond transferring risks onto foreign suppliers, many large companies with complex supply chains are also divesting or restructuring WFOEs, JVs, and sourcing offices in favor of more flexible platforms such as contract manufacturers and outsourced service providers. This can reduce direct regulatory exposure and improve operational flexibility.

From an economic and demographic perspective, companies that historically relied on China’s low-cost labor base have increasingly shifted incremental sourcing toward emerging markets such as India, Vietnam, Thailand, and Malaysia—a trend that has accelerated since 2016.

Those opting to remain in China are still taking various mitigation steps from qualifying secondary sources within and outside the country, mapping sub-supplier networks, reviewing IP and tooling ownership, and seeking to implement various improvement initiatives and technologies to increase efficiencies.

Most companies recognize the risk—but few successfully execute diversification at scale.

-

Diversification is often discussed but rarely executed

-

Internal teams lack time to pursue new markets

-

Efforts stall before reaching production

-

Risk remains—despite awareness

Retention

Lastly, some companies are deliberately choosing to retain exposure to China despite the associated risks. These companies usually have difficulty finding a comparable supply base for their product in other markets, switching costs are prohibitive, or they require in-market manufacturing to support export sales to the region.

In these cases, companies are wide-eyed on the current risk landscape, acknowledge the challenges ahead and continue to take proactive measures to manage exposure.

Conclusion – The Shift from Cost Arbitrage to Resilience Engineering

Ultimately China has not become unviable — but the structural conditions that once made single-country concentration an obvious choice have materially changed. Regulatory friction, geopolitical uncertainty, economic headwinds, and demographic shifts have altered the risk-adjusted return profile of China-centric supply chains.

For many industries, China will remain indispensable. Its supplier ecosystems, infrastructure, and technical capabilities cannot be replicated overnight. However, high concentration is no longer a default operating posture. It is a deliberate strategic choice.

Supply chain architecture is not solely a procurement exercise focused on lowest landed cost. It is an enterprise-level decision tied to margin durability, ROIC stability, working capital resilience, and operational optionality.

The question facing executives is not, “Should we be in China?” It is, “Are we comfortable with our current exposure to China?”

The question facing executives is not, “Should we be in China?” It is, “Are we comfortable with our current exposure to China?”

Over the last two decades, competitive advantage was built on efficiency and cost arbitrage. In the decade ahead, advantage will increasingly be tied to organizations that engineer resilience into their operating models balancing efficiency with optionality, and growth with disciplined exposure management.

The companies that proactively recalibrate their concentration risk will not simply avoid disruption, they will operate from a position of strategic flexibility in a structurally more volatile global environment.